2008年08月04日

課題2終了

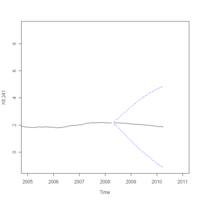

貸出約定平均金利

期間 76年1月~08年5月

Call:

arima(x = ty1, order = c(2, 1, 2), seasonal = list(order = c(1, 1, 1), period = 12))

Coefficients:

ar1 ar2 ma1 ma2 sar1 sma1

0.5786 0.2370 0.6585 0.0780 -0.0794 -1.000

s.e. 1.9459 1.6442 1.9536 0.8001 0.0523 0.045

sigma^2 estimated as 0.001744: log likelihood = 636.22, aic = -1258.43

期間 76年1月~08年5月

Call:

arima(x = ty1, order = c(2, 1, 2), seasonal = list(order = c(1, 1, 1), period = 12))

Coefficients:

ar1 ar2 ma1 ma2 sar1 sma1

0.5786 0.2370 0.6585 0.0780 -0.0794 -1.000

s.e. 1.9459 1.6442 1.9536 0.8001 0.0523 0.045

sigma^2 estimated as 0.001744: log likelihood = 636.22, aic = -1258.43

Posted by ikumi at 13:06│Comments(0)